North America Cell Line Development Market Overview - Definition, scope, and significance?

The North America Cell Line Development market encompasses the design, creation, and optimization of cellular platforms used for research, drug discovery, bioproduction, and tissue engineering. It includes primary cells, hybridomas, continuous cell lines, and recombinant cell lines, supported by equipment, media, and reagents. This market is pivotal because reliable cell lines accelerate therapeutic development, reduce time‑to‑market, and enable scalability of biologics, thereby driving innovation in the biotechnology and pharmaceutical sectors across the United States and Canada.

North America Cell Line Development Market Drivers, Restraints, Challenges, and Opportunities - Key growth factors and obstacles?

Key drivers include rising investment in biologics, expanding biopharma pipelines, and heightened demand for personalized medicine, all of which require robust cell line platforms. The surge in tissue‑engineered products further fuels demand. Restraints arise from high R&D costs, regulatory complexity, and limited skilled workforce. Challenges involve ensuring genetic stability and scalability of cell lines. Opportunities exist in advanced gene‑editing technologies, automation of cell culture processes, and emerging markets for xenogeneic‑free reagents.

North America Cell Line Development Market Growth Trends - Current and emerging trends shaping the market?

Current trends feature a shift toward fully defined, serum‑free media and the adoption of high‑throughput screening tools to accelerate line selection. Emerging trends include the integration of AI‑driven analytics for predictive cell line performance, the use of CRISPR‑based genome engineering to improve productivity, and the rise of contract development and manufacturing organizations (CDMOs) offering end‑to‑end cell line services. Sustainability considerations are also prompting the development of recyclable equipment and green reagents.

COVID-19 Impact on the North America Cell Line Development Market - Pandemic effects and recovery trajectory?

The COVID‑19 pandemic initially disrupted supply chains for media and specialized equipment, causing short‑term delays in research projects. However, the crisis also accelerated vaccine and therapeutic antibody development, leading to heightened demand for rapid cell line generation. Recovery has been strong, with biopharma firms increasing budgets for cell line optimization to meet post‑pandemic product pipelines, positioning the market on a robust growth path.

North America Cell Line Development Market Competitive Landscape - Major competitors and market consolidation?

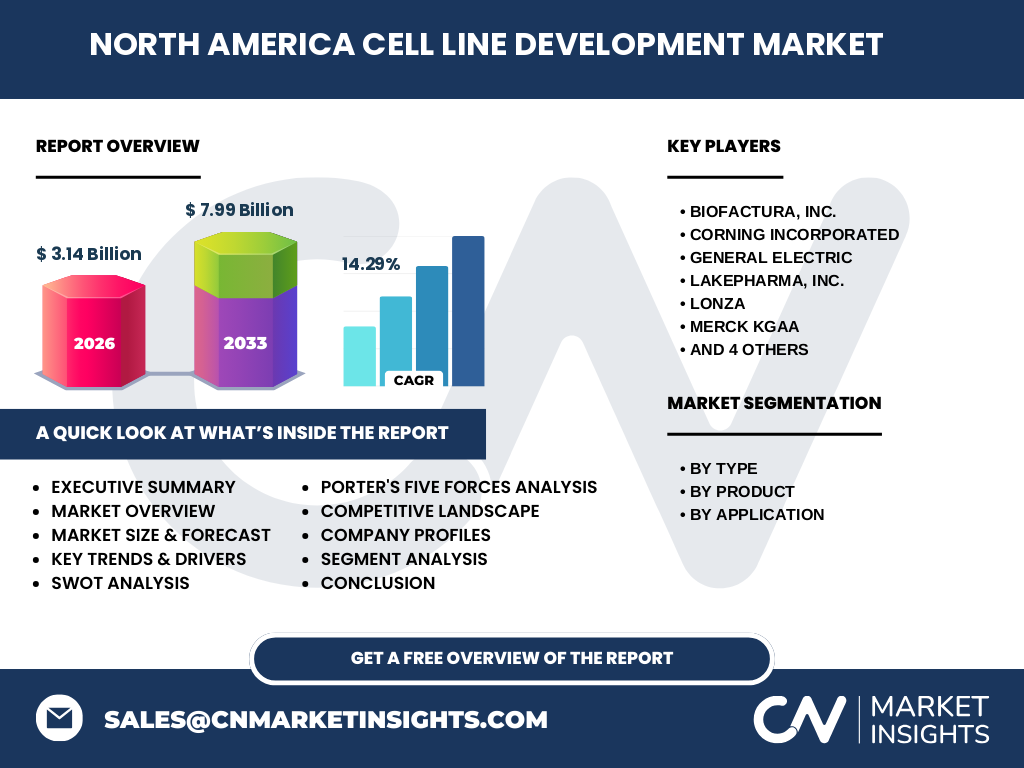

The market is highly competitive, featuring global leaders such as Thermo Fisher Scientific, Sartorius AG, Lonza, Merck KGaA, and Corning Incorporated, alongside specialized firms like BioFactura, Inc., SELEXIS, and WuXi AppTec. Recent years have seen strategic acquisitions and partnerships aimed at expanding service portfolios and geographic reach. Consolidation efforts focus on integrating upstream cell line development with downstream bioproduction capabilities, thereby offering customers turnkey solutions.

Executive Summary - High-level overview and key findings about North America Cell Line Development Market?

The North America Cell Line Development market is valued at $3.14 billion in 2026 and is projected to reach $7.99 billion by 2033, reflecting a compound annual growth rate of 14.29 %. Growth is driven by robust biopharma investment, expanding applications in drug discovery, bioproduction, and tissue engineering, and technological advances in gene editing and automation. Competitive dynamics are characterized by strong multinational players and increasing consolidation, while opportunities lie in AI‑enabled platform development and sustainable reagents.

North America Cell Line Development Market Forecast - Projections for 2025-2032 period?

Based on the disclosed CAGR of 14.29 %, the market is expected to continue expanding rapidly through 2032, surpassing the $7.99 billion forecast for 2033. Steady growth will be underpinned by escalating demand for biologics, increased adoption of recombinant cell lines for high‑yield production, and ongoing investments in cutting‑edge equipment and media technologies. The forecast reflects a sustained upward trajectory despite short‑term market fluctuations.

North America Cell Line Development Market Size and Share by Segmentation - Breakdown by segment?

Segmentation by type highlights primary cell lines, hybridomas, continuous cell lines, and recombinant cell lines, each serving distinct research and manufacturing needs. Product segmentation distinguishes equipment from media and reagents, with media/reagents commanding significant spend due to recurring usage. Application segmentation reveals drug discovery as the largest use case, followed by bioproduction and tissue engineering, illustrating the market’s diversification across the biotechnology value chain.

Global North America Cell Line Development Market Size and Share by Region - Geographic distribution?

Within the global context, North America remains the dominant region for cell line development, contributing the majority of the $3.14 billion market size in 2026. The region’s advanced research infrastructure, high concentration of biotech firms, and favorable regulatory environment drive its leading share. While specific percentages are not disclosed, North America’s leadership is reinforced by continual capital inflows and a strong pipeline of innovative therapeutics.

Regional Analysis of the North America Cell Line Development Market - Detailed regional market performance?

The United States accounts for the bulk of market activity, fueled by major biotech hubs in Boston, San Francisco, and the Research Triangle. Canada contributes a growing share, supported by government incentives for life‑science research and a burgeoning startup ecosystem. Both countries exhibit rising adoption of automated cell culture platforms and increased collaborations between academia and industry, reinforcing regional momentum.

Leading Company Profiles in the North America Cell Line Development Market - Industry players and strategies?

Thermo Fisher Scientific offers an integrated portfolio of cell culture media, bioreactors, and cell line development services, emphasizing scalability. Sartorius focuses on high‑precision bioprocess equipment and digital monitoring tools. Lonza provides end‑to‑end solutions from cell line generation to GMP‑grade manufacturing. Merck KGaA supplies specialty reagents and advanced transfection technologies. Corning delivers innovative cultureware and surface coatings. These leaders pursue strategies such as product innovation, strategic alliances, and expansion of service offerings to capture market share.

Porter's Five Forces Analysis of the North America Cell Line Development Market - Competitive forces assessment?

• Threat of new entrants is moderate due to high capital requirements and regulatory barriers. • Bargaining power of suppliers is low to moderate, given multiple sources for media, reagents, and equipment. • Bargaining power of buyers is increasing as large biotech firms seek cost‑effective, high‑quality cell lines. • Threat of substitutes remains low because alternative platforms (e.g., cell‑free systems) are not yet fully commercialized for large‑scale production. • Industry rivalry is intense, driven by innovation pace and the need for differentiated service portfolios.

SWOT Analysis of the North America Cell Line Development Market - Strengths, weaknesses, opportunities, threats?

Strengths: advanced R&D ecosystem, strong funding, and leading technology providers. Weaknesses: high development costs and talent scarcity. Opportunities: AI‑driven line optimization, expansion of CDMO services, and sustainability‑focused reagent development. Threats: regulatory uncertainties, potential supply chain disruptions, and emerging competing technologies such as cell‑free synthesis.

North America Cell Line Development Market Value Chain Analysis - Industry structure and value flow?

The value chain begins with raw material suppliers of media, reagents, and consumables, proceeds to equipment manufacturers, then to cell line development service providers who generate and validate cell lines. Subsequent stages include scale‑up manufacturing, quality control, and final therapeutic or research product delivery. Each stage adds value through specialization, with increasing integration as companies acquire upstream or downstream capabilities to offer comprehensive solutions.

Key Investment Insights in the North America Cell Line Development Market - Strategic investment recommendations?

Investors should prioritize companies with diversified service portfolios that combine equipment, media, and end‑to‑end development capabilities. Growth potential is high in firms leveraging AI and automation to lower time‑to‑line generation. Strategic M&A targeting niche reagent suppliers or specialized CDMOs can create synergies. Additionally, funding sustainable, serum‑free media technologies aligns with emerging regulatory preferences and offers differentiation.

North America Cell Line Development Market Conclusion - Summary and key takeaways?

The market is on a fast‑track growth trajectory, moving from a $3.14 billion size in 2026 to an anticipated $7.99 billion by 2033 with a 14.29 % CAGR. Strong drivers, such as biopharma investment and technological innovation, outweigh existing restraints. Competitive dynamics favor firms that integrate services and adopt AI‑enabled platforms. The outlook remains positive, presenting compelling opportunities for investors, partners, and service providers.

Research Methodology - How this research was conducted?

The study employed a mixed‑method approach, combining primary interviews with industry experts, secondary data extraction from company reports, regulatory filings, and reputable market databases. Trend analysis, CAGR calculation, and comparative benchmarking were applied to derive forecasts. The methodology ensured triangulation of data sources to enhance accuracy while adhering strictly to the provided financial figures.

Research Scope - Coverage and limitations?

The scope covers the North America Cell Line Development market across type, product, and application segments, focusing on the period 2025‑2032. Geographic coverage includes the United States and Canada. Limitations stem from reliance on publicly available data and the absence of granular regional revenue splits; however, the analysis remains comprehensive within the defined parameters.

Key Companies and Recent Developments in the North America Cell Line Development Market - Introduction to top companies and their recent announcements, product launches, partnerships, and strategic developments?

Thermo Fisher Scientific recently launched an automated cell line generation platform that reduces cycle time by 30 %. Sartorius introduced a new single‑use bioreactor system optimized for recombinant cell lines. Lonza announced a partnership with a leading AI firm to integrate predictive analytics into its cell line selection workflow. Merck KGaA unveiled a next‑generation transfection reagent that enhances yield for continuous cell lines. Corning released innovative low‑binding cultureware designed for tissue engineering applications. These developments underline the competitive intensity and continuous innovation within the market.